It is incredibly easy to look back with 20/20 hindsight and critique corporate history. But this isn’t a post-mortem. This is a diagnostic warning for every CEO, CMO, and growth executive currently prioritizing short-term capital efficiency over holistic growth sequencing. If your head is buried strictly in localized channel P&L sheets, you might be funding your own disruption.

The story begins with a legendary data science victory. Locked in a fierce market share battle with Lyft, Uber’s growth analytics team, spearheaded by former data science head Sundar Swaminathan, moved away from lazy, click-based last-touch attribution models. They implemented rigorous, three-month localized incrementality testing on their heaviest performance channels, specifically targeting Meta ads across the US and Canada.

The data returned an undeniable truth: their paid social spend was almost entirely non-incremental. Major urban centers were completely saturated, meaning the ads were simply bidding on riders who were already organically hardwired to open the app. When they paused the spend, acquisition volume didn't budge.

Uber made the objectively correct, data-driven decision: they shut off the non-incremental spend, saving a clean $35MM. Coupled with a massive $100MM pullback after uncovering global ad fraud, Uber suddenly recaptured $135MM in absolute waste.

On paper, it was a masterclass in capital efficiency. Finance cheered. The data team was validated. And the macro strategy seemed sound: Uber didn't just pocket the cash; they aggressively reinvested it directly into global expansion, driver supply acquisition, and Uber Eats.

So how, with an optimized data stack and a nine-figure war chest explicitly funneled into delivery, did Uber Eats completely lose the US market to a quiet challenger?

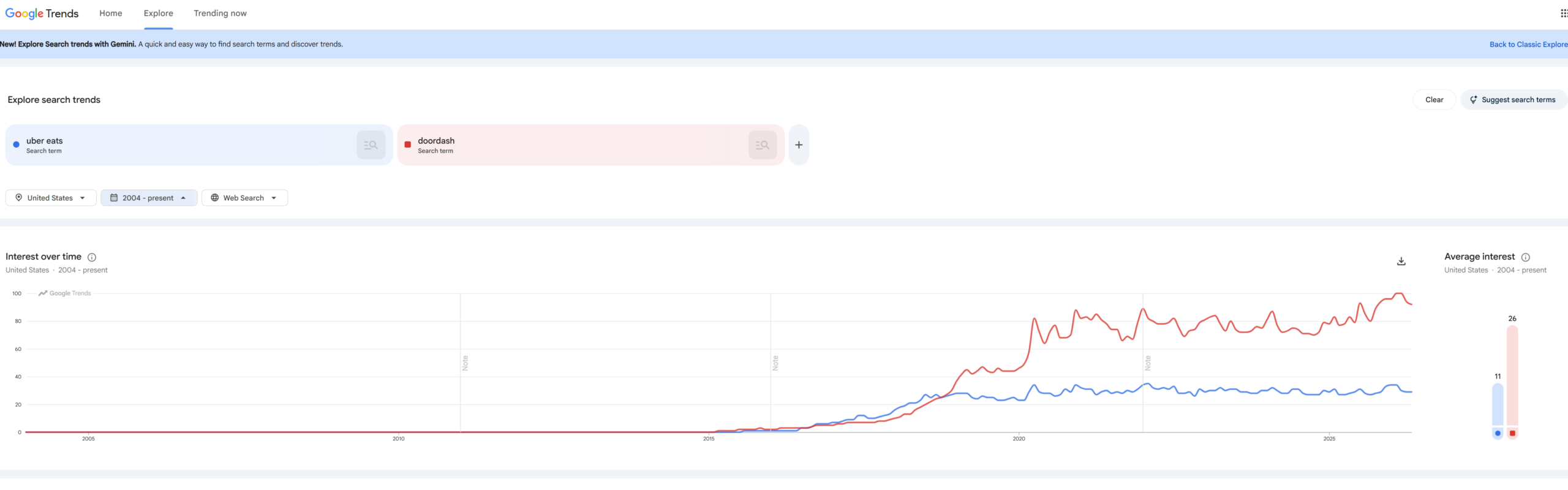

The Crossover: Visualizing the Vacuum

Look at the Google Trends search data from that exact optimization window, and the operational blind spot becomes glaringly obvious.

Up until mid-2018, Uber Eats and DoorDash were locked on the same growth trajectory. But as Uber focused heavily on local cost-per-acquisition (CPA) efficiency and channel-siloed incrementality, they completely pulled their foot off the gas in defensive, high-intent performance channels like paid search.

During the week of September 30 to October 6, 2018, the lines intersected. DoorDash officially crossed Uber Eats in US search interest. Immediately following that crossover, the trajectories permanently decoupled: Uber Eats completely plateaued into a flat line, while DoorDash entered an explosive, near-vertical breakout.

DoorDash didn't win because they had a prettier logo or a superior high-concept brand narrative. They won because they understood the structural mechanics of a two-sided marketplace network effect. Coupled with Uber’s efficiency vacuum, they were able to inadvertently stumble on a way to fund their way to marketshare.

1. The Paid Search Conquest Trap

When a dominant market player pulls back on defensive paid search and performance channels, high-intent consumer demand doesn't vanish from the internet. The keywords "food delivery near me" still get typed into Google millions of times a day. The only difference is that the auction traffic suddenly becomes dramatically cheaper and entirely uncontested for everyone else.

DoorDash didn't just fill that vacuum; they aggressively bankrolled it. Every high-intent customer Uber decided was "too expensive" or "non-incremental" on a spreadsheet was instantly bought up by DoorDash. Because food delivery is a high-habit, high-frequency utility, it wasn't a one-off transactional acquisition. It was a permanent deflection of customer Lifetime Value (LTV). DoorDash literally weaponized Uber's localized efficiency wins to fund its own long-term market acquisition engine.

2. The Suburban Food Desert Strategy

Uber’s data team correctly identified that major US urban centers were fully saturated for their rideshare business. They fundamentally assumed that because their brand was completely ubiquitous in tier-1 cities, urban density would automatically translate into delivery dominance.

DoorDash spotted the structural blind spot to survive Uber's onslaught through intentionality. They were able to bypass the hyper-expensive, low-margin urban dogfights entirely and systematically captured suburban America.

They targeted the "suburban food deserts" geographies where families order high-ticket, multi-person meals instead of a single corporate lunch salad. By the time Uber realized that suburban regions yielded dramatically higher Average Order Values (AOV) and vastly stickier user retention profiles, DoorDash had constructed an unshakeable supply-side fortress of exclusive local restaurant partnerships and driver network density.

The Executive Lesson: Brand and Performance Are a Continuous Ecosystem

This is where the standard, exhausted debate between brand storytelling and growth marketing completely goes off the rails.

Uber viewed performance marketing through a narrow, siloed lens as an adjustable acquisition expense to be optimized for localized unit economics. In doing so, they completely missed its defensive value in protecting marketplace liquidity and network velocity. They won the localized margin fight but permanently ceded the category footprint.

DoorDash understood the reality of the sequence:

- Performance marketing buys the initial geographical footprint and supply density.

- Supply density drives the marketplace liquidity and organic utility.

- Marketplace liquidity finally earns the brand the right to tell a bigger, emotional story.

If your executive leadership team is currently treating performance marketing and brand equity as competing line items on a spreadsheet rather than a tightly sequenced, interdependent ecosystem, you aren't being efficient. You are simply leaving the door wide open for a challenger to take your market.